Some investors are realizing that traditional methods of mitigating risk such as spreading holdings across more geographic regions or sectors or balancing their portfolios between equities and fixed income may not have the level of diversification they want.

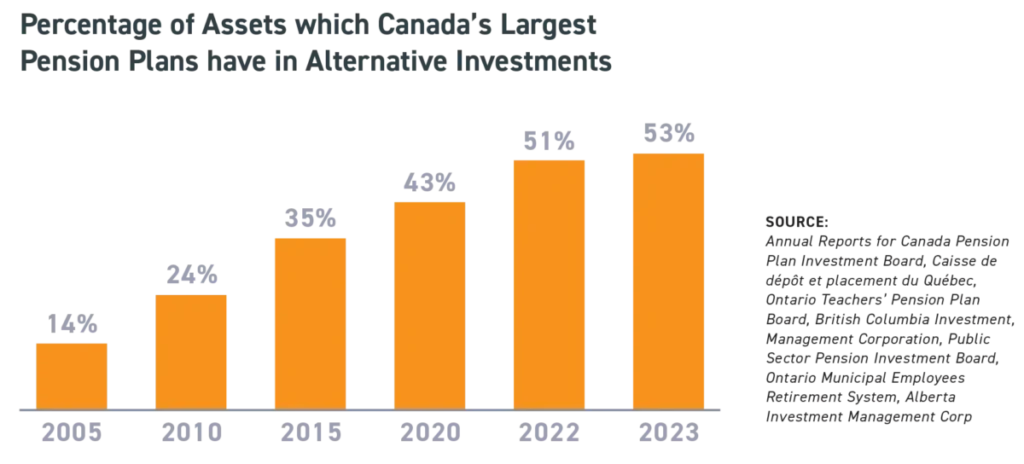

Working toward this objective, the Maple Eight began to diversify into alternative investments — financial assets that don’t fit into conventional investment categories — in the 1990s and have continued that trend over time. Alternative investments can include private equity or venture capital, hedge funds, commodities, and private real estate funds.

Tellingly, over the last 20 years, North America’s CPP, OMERS, OTPP, CalPERS, Yale Endowment, and Harvard Endowment have all substantially increased their relative holdings in real estate and other alternative investments to reduce the overall volatility and increase the returns of their investment portfolios. Omitting the holdings of Healthcare of Ontario Pension Plan (the smallest of the Maple Eight), Canada’s seven largest pension plans dramatically increased the share of alternative assets within the C$1.7T they manage.

Private real estate funds tend to focus on specific property types, offering investors tailored exposure to a variety of assets. Private rental apartment funds focused on residential income-producing properties have long been a popular choice, and for good reason.

In addition to diversification, private rental apartment funds typically aim to provide investors with regular income and capital appreciation opportunities. With these benefits, investors should be aware that private alternative investments come with liquidity-, transparency-, and management-related risks.

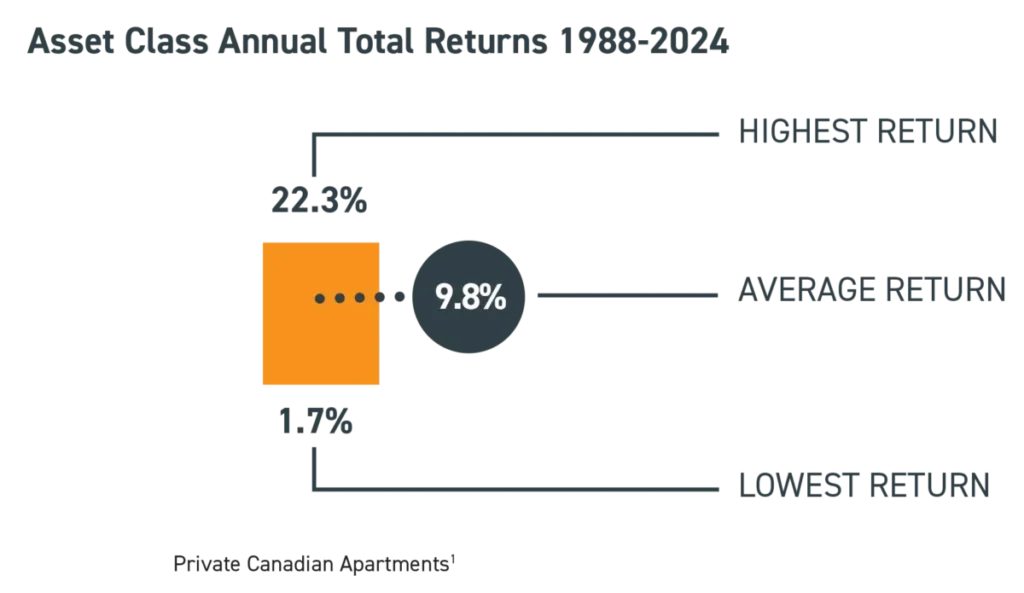

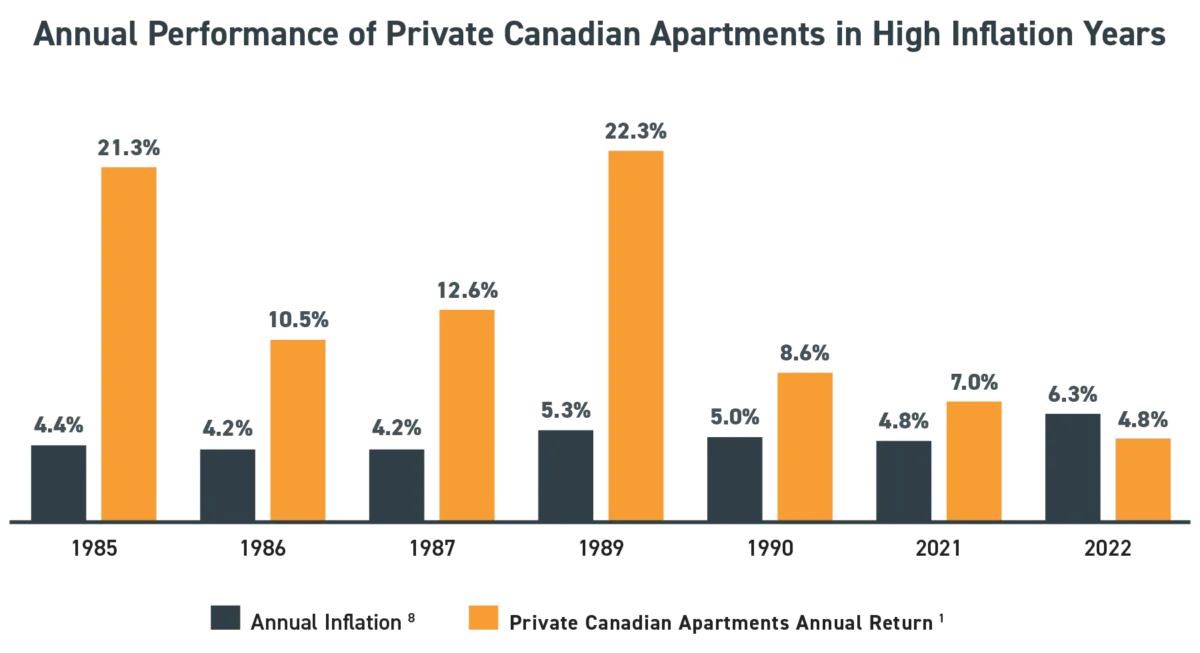

As illustrated above, the Private Canadian Apartments Index has yet to record a year without positive returns since its creation in 1985. Although this measure does not guarantee future performance, it helps demonstrate the resilience of the index’s underlying asset class across various market cycles, including the Financial Crisis of 2008-2009 and the COVID-19/Inflation Crisis.

This includes the challenging period from 1986 to 1991 when the index delivered between 8.6% and 22.3%, significantly outpacing inflation.

Distributions received from a rental apartment fund can be more tax efficient than other forms of income in a non-registered account, creating opportunities for long-term tax planning and smart wealth generation. Of course, an individual investor’s choice of investment will depend on many factors, including their risk comfort level and investment objectives. Different investment assets are characterized by varying levels of risks and returns. Tax efficiency is one criterion we can examine.

To explore the tax efficiency of some popular sources of investment income, compare the tax treatment of $100,000 allocated to an investment yielding a 6% dividend, an interest-paying investment yielding 6%, or a rental apartment fund with a 6% distribution.

An investor in a rental apartment fund with a 6% distribution may be able to defer paying any tax until the investment is sold, assuming the fund is 100% tax efficient and classifies all its distributions as return of capital (ROC). ROC occurs when a rental apartment fund distributes amounts sourced from an investor’s original investment, rather than from income or profits.

From an after-tax cash flow perspective, the dividend-paying investment would generate $362 every month while the interest-bearing investment would generate $275. The investor in the rental apartment fund would receive $387.50 monthly if the distributions were fully taxed that year or a full $500 if distributions were classified as 100% ROC.

In this way, an investor who chooses tax-efficient investments in private rental apartment funds to generate cash flow can potentially free up a substantial amount of capital, which can be deployed elsewhere or reinvested to accelerate the effects of compounding.

Q1 2024 Commentary and Outlook – A Turning Point for Rentals?